How is the industrial real estate market doing in the Moravian-Silesian Region?

3. 2. 2021Last year, the Czech economy experienced the biggest decline in history. According to preliminary estimates by the Czech Statistical Office, gross domestic product decreased by 5.6 %. A further decline was prevented by a well-functioning industry driven by foreign demand and, in part, by the government economic programs.

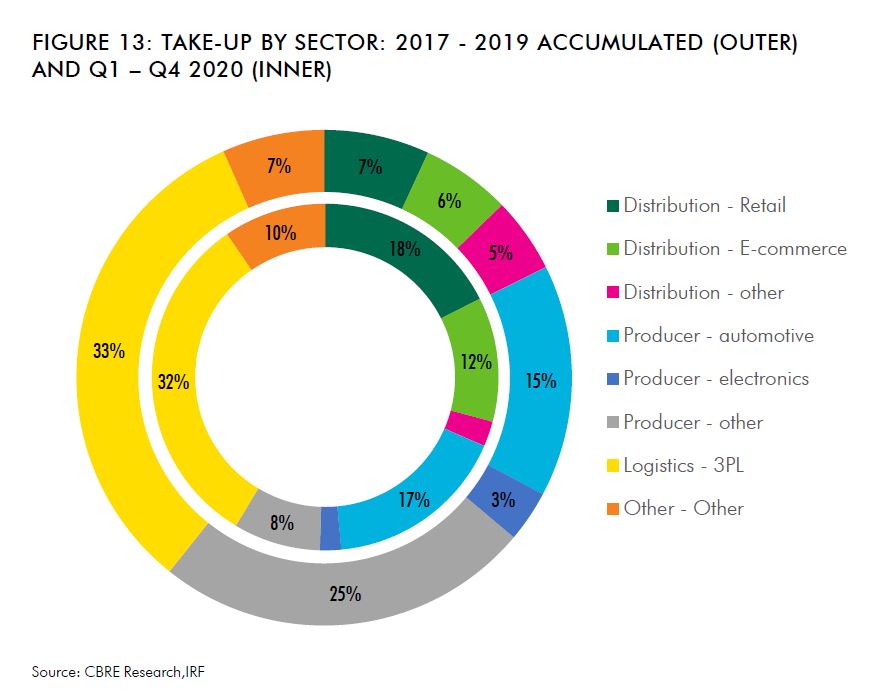

How did the industrial real estate market react to the economic decline last year? The real estate market changed dramatically last year and developers as well as tenants across all industries had to rethink their needs and focus on maximum efficiency and productivity. The industrial and logistics real estate market performed relatively well despite the circumstances. Almost 670,000 sq m of industrial and logistics halls were completed last year, which represents a 10 % year-on-year increase. At the beginning of the coronavirus pandemic, there was a significant slowdown in the real estate market, forcing tenants to negotiate new conditions, which resulted in a rent freeze in the second quarter of 2020. This, in turn, caused an unprecedented take-up at the end of the year, when leases concluded or extended made a total of 355,000 sq m. The main reasons behind such demand were the retail and e-commerce sectors and, to a large extent, the automotive industry. Out of the total of newly rented premises, more than a quarter was made up of the manufacturing industry, of which about a quarter was the automotive sector. The strong role of the automotive industry is also expected in the future thanks to the onset of electromobility.

Approximately 340,000 sq m is currently under construction, with delivery expected in 2021, of which 70 % has been already pre-leased. In total, it is calculated that 700,000 - 800,000 sq m of industrial and logistics halls should be added to the market this year. The share of speculative construction decreased from 34 to 30 % at the end of last year; however, in larger cities such as Prague, Brno or Ostrava, it should remain above average. The attractiveness of Ostrava and its surroundings is also reflected in the fact that almost one fifth of the areas under construction are in the Moravian-Silesian Region. The largest transaction in the fourth quarter of 2020 was a pre-lease in Contera Park Ostrava D1 in a size of 74,000 sq m. The largest completed building was a hall in CTPark Ostrava with an area of 50,000 sq m. Compared to the same period in 2019, the highest rent of industrial and logistics real estate stagnated in the range between 4.50 and 4.85 EUR/sqm/month. In comparison with the three largest Czech cities, Ostrava maintained an average rent in the range between 4.00 and 4.35 EUR/sqm/month. Compared to the rest of the Czech Republic, the Moravian-Silesian Region offers the widest range of large retail projects of up to 100,000 sq m. These projects can be attractive, for example, for central distribution warehouses and for e-commerce. One of the specifics of the region is also that it is possible to build halls up to 25 meters high, which is a unique asset.

Sources: CBRE Market Outlook, Colliers, CSO